How to Calculate Net Worth: The One Calculation That Shows If You Are On Track

You work hard. You pay your bills on time. You are not reckless with money. And yet, there is this persistent, low-grade question that follows you around: Are we actually on track? If that question sounds familiar, you are not alone. You are not doing anything wrong. You don’t need more discipline or more income. What you are missing is a clear financial snapshot. Calculating your net worth is the fastest, most clarifying number you can know. Once you see it, you will finally have something concrete that tells you whether your money decisions are keeping you on track and moving in the right direction.

What is Net Worth, and Why Does It Matter?

Net worth is simply the sum of everything you own minus the sum of everything you owe. That is it. No complicated formula. No financial degree required.

Positive net worth means your assets outweigh your debts.

A negative net worth means you owe more than you own. And that is more common than you think, especially earlier in a career.

What makes this number so powerful is not where it is right now -- it is where it is heading. Your net worth is a living, trackable measure of your financial direction. Think of it like a financial GPS. You do not just need to know your destination; you need to know whether you are moving toward it or away from it. Net worth tells you exactly that.

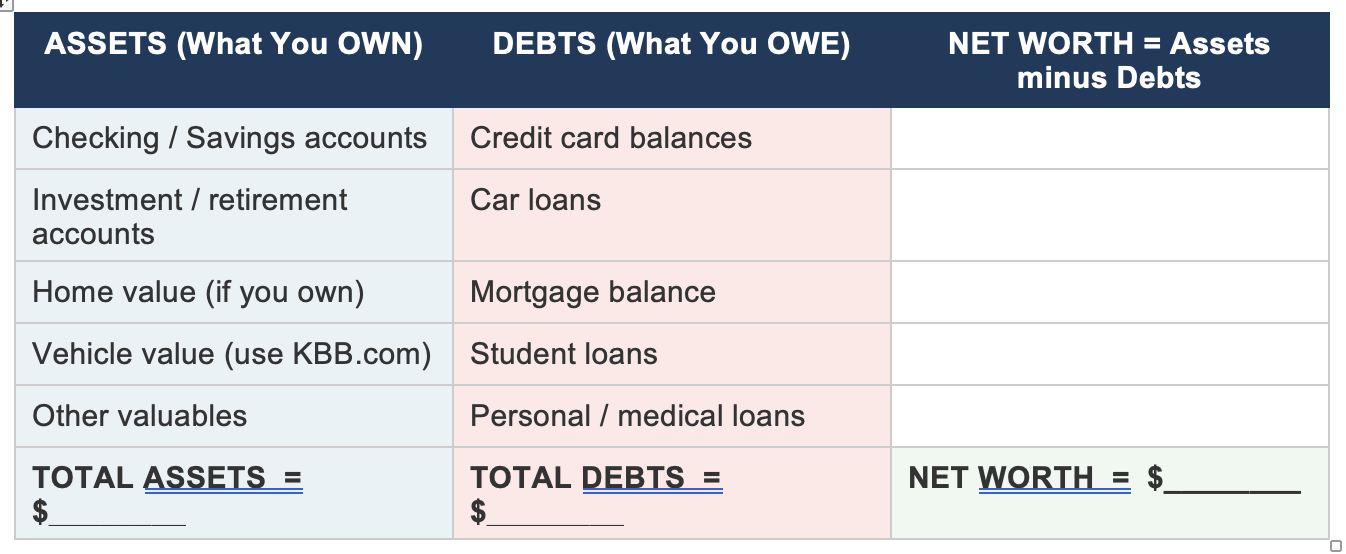

How to Calculate Your Net Worth: A Simple Step-by-Step

Step 1: Add Up Your Assets

Assets are everything you own that has financial value. Do not overthink this -- just list what applies to you:

Checking and savings account balances

Investment and retirement accounts (401k, IRA, brokerage)

Your home's current market value (if you own)

Vehicle value -- use KBB.com (Kelley Blue Book) to get an accurate current number

Other valuables: jewelry, business equity, rental property

Step 2: Add Up Your Debts

Debts are every dollar you owe to someone else:

Credit card balances

Car loan balances

Mortgage remaining balance

Student loan balances

Personal loans or medical debt

Step 3: Subtract Debts from Assets

Use this simple worksheet to get your number right now. Replace the item in the list with your actual amount and put the sum at the bottom.

Knowing the number, no matter how good or bad, is always better than not knowing. Your net worth today is simply your starting line. You cannot steer in the right direction without first knowing where you stand.

The Strategy is Simpler Than You Think

Minimize Debts. Maximize Assets

Here is the principle that shapes everything in smart personal financial planning: Minimize debts. Maximize assets. When you commit to that two-sided strategy, your net worth can only move in one direction up.

On the asset side, maximizing means consistently contributing to your retirement accounts, building your savings, and paying cash for big purchases and replacement items by saving for them in advance rather than financing them. Paying cash for what you can keeps money on your side of the ledger.

On the debt side, minimizing means paying off existing balances, avoiding new consumer debt, and making every dollar you owe a shrinking target. The less you owe, the more of your income stays available to build the asset side.

The real power of this strategy shows up when you track all three numbers (your assets, your debts, and your net worth) over time. Checking in monthly or quarterly lets you see which side of the strategy is working and which needs more attention. That visibility tells you exactly where to focus your energy. You do not have to do both perfectly at once. The goal is consistent, measurable movement in the right direction.

What is Compound Interest? (And Why It Changes Everything)

Compound interest is the most powerful force in personal finance. And it works in both directions. With simple interest, you earn or pay interest only on the original amount. With compound interest, you earn interest on the original amount plus all the interest already earned. The balance grows faster every year because the interest itself starts earning interest.

When you invest, this force builds your wealth. When you carry debt, it builds your balance due. The minimize debts, maximize assets strategy puts compound interest to work on your side.

Interest Working For You: Building Wealth While You Sleep

When you maximize assets by investing, you are doing something remarkable: you are setting aside money and letting it earn money for you without trading your time for it. That is the asset side of the strategy in action.

Notice how the interest earned each year keeps growing. In Year 5, the investment earns $92. By Year 30, that same investment earns $497 in a single year without any additional contribution. The money is doing the work.

By Year 30, $6,612 of that $7,612 balance came purely from interest for 87% of the total. You contributed $1,000. Interest contributed the rest.

Time is the ingredient.

The earlier you start, the more interest works for you. Every year you wait is a year of compounding you cannot get back.

To maximize the asset side of your net worth, you need margin (money left over after your obligations are met) to set aside for investing. That is one more reason why minimizing debts matters so much. The sooner a debt is eliminated, the sooner that payment amount can move from the debt side to the asset side.

Why Debt Is Costing You More Than You Realize: Interest Working Against You

When you carry debt, that same powerful compound interest runs in reverse. You pay interest on what you owe, and the balance resists going down, especially when payments are small.

Here is what $1,000 in debt actually costs depending on your interest rate and payment:

What the Table Is Really Showing You

The 0% row looks clean, but you still carry debt for 10 months with $100 tied up every month.That is money that cannot go toward savings or anything else you want. At 5 to 22% APR with a $100 payment, the extra cost is modest with roughly one extra month and a small interest charge.

The dramatic shift is the last row. At 29% APR with a $30 minimum, the same $1,000 takes 54 months to pay off and costs $607 in interest alone. Why? In the early months, most of the minimum payment goes straight to interest, barely touching the balance. By the time the debt is gone, whatever you bought is likely worn out or gone and you have been paying for it for four and a half years. That is the river current working against you. Eliminating debt removes it entirely.

The Small Habit With Big Impact: Track Your Net Worth Over Time

Calculating your net worth once is valuable. Tracking it over time is transformational. When you check in monthly or quarterly, you stop guessing about your financial progress and start seeing it in black and white. Annual check-ins are too infrequent. You lose the momentum that comes from watching the numbers move.

A few simple habits make this tracking easy:

Set a recurring calendar reminder to update your numbers once a month or once a quarter

Keep a simple spreadsheet with your asset totals, debt totals, and net worth by date

Look for two things each time: Is the asset column growing? Is the debt column shrinking?

If either side is going the wrong direction, that tells you exactly where to focus your energy next.

Celebrate the direction, not just the destination.

You do not need a perfect number. You need a moving-in-the-right-direction number. Even small improvements like a retirement contribution made, a credit card balance reduced, a savings account that grew will show up here. And seeing that progress consistently is what keeps you motivated and confident.

For mid-career professionals especially, this kind of financial clarity is life changing. It is the difference between wondering if you could ever work less, travel more, retire when you want, or change careers and actually knowing whether the math supports it.

What Financial Clarity Actually Makes Possible

When you know your net worth and you are watching it grow, something shifts. You move from reactive to intentional. From anxious to confident. From paycheck-focused to lifestyle-focused. You allow yourself to dream again.

Here is what that looks like in practice:

You can answer "Can we affort this?" with data, not anxiety.

You become more aware of your spending and find natural ways to avoid taking on more debt.

You can evaluate a career change, reduced hours, or retirement, because you understand your financial runway.

You can spend on what matters (travel, family, experiences) without guilt, because your plan accounts for it.

Financial confidence is not about having a perfect financial life. It is about having clarity and knowing where you stand, understanding where you are headed, and trusting the plan that is moving you there.

Your net worth is the foundation of that clarity. And it starts with a number you can calculate today.